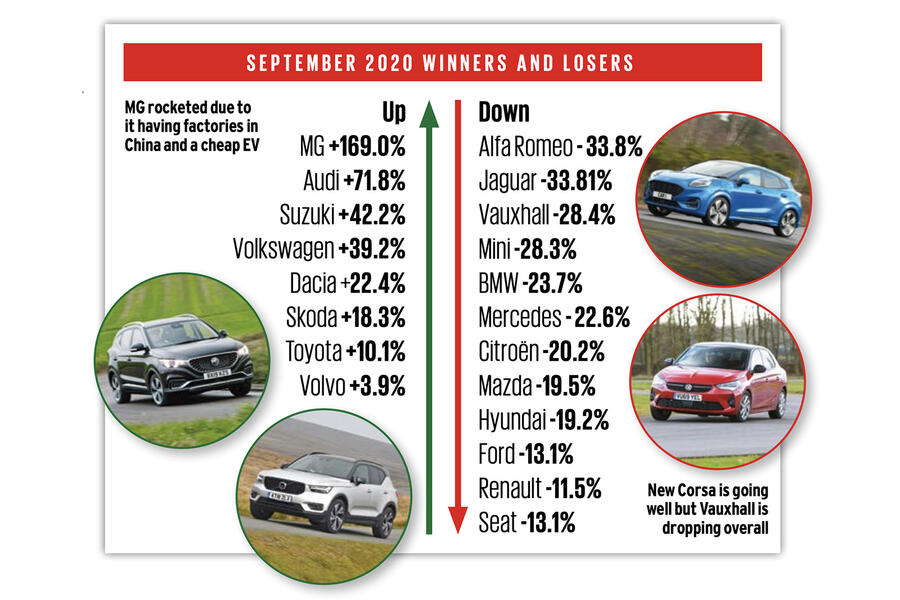

Given the negativity that has ravaged the car industry this year, the Society of Motor Manufacturers and Traders’ (SMMT) commentary on the 4.4% drop in year-on-year UK new car registrations for September – traditionally the second-strongest month of the year, due to the plate change – was appropriately downbeat.

SMMT chief executive Mike Hawes underlined this mood, emphasising the worst September sales performance this century: “During a torrid year, the automotive industry has demonstrated incredible resilience, but this isn’t a recovery. Despite the boost of a new registration plate, new model introductions and attractive offers, this is still the poorest September since the two-plate system was introduced in 1999.”

It was this position that led the national headlines, the bad news further exaggerated by the knowledge that September 2019 had itself been deemed extremely disappointing, due to some key manufacturers – led by Volkswagen Group brands – not having enough WLTP-emissions-compliant stock ready for customers.

The gloom was based on inarguable registrations data and backed by the prediction that the year will now end 30.6% down from 2019 – a fall of 708,000 units. That’s an estimated loss of £21.2 billion of sales based on industry analyst JATO Dynamics’ estimation that the average car in the UK is sold for £30,000.

However, the SMMT position tells only one side of the story. In total contrast, talking to a wide range of retail group leaders both on and off the record, Autocar received universal reports of a month of resounding sales success.

“Trading conditions were as strong as I can remember. For us at least, it was a record month for profitability, and it’s possibly the case for the industry as a whole, I would think,” said Robert Forrester. He’s the boss of Vertu Motors, the fifth-largest franchised dealer group in the UK, with more than 120 different outlets spanning mainstream and premium brands, as well as one of the largest commercial vehicle retailers in the UK.

Join the debate

Add your comment

Available stock

I can't help but wonder if sales are up but deliveries are down/very slow due ot limited factory output. Can't really tell from this article though.

Surprising...

What rubbish!

Autocars liking of the meaningless article knows no bounds.

Obviously from the figures, the car market for this year is well down overall. However, the industry has structured itself round two periods, March/April and September/October, and secured a baseline load with PCP deals which often require renewal at these times.

It is therefore no surprise that sales in September/October this year are much less down than any time since March. Also, there is some truth I would guess with people spending less on holidays abroad and hospitality, that some are treating themselves to a new car.

The really interesting period will come between now and next March, when the twin headwinds of the pandemic continuing to bite on incomes (never mind predicted job losses) and possible Brexit induced tariffs will really hit the industry and new car retailers.

Personally I have just negotiated an excellent deal on a new car, so am certain that discounts are very much alive and well at most retailers and they are fairly desperate for new sales, (particularly ex-stock rather than factory order).

Already the usual suspects like Honda/Mazda/Seat/Citroen etc are offerring enhanced deposit contributions and low finance and I can only see that increasing into next year as long as factories continue production.